If you’re hoping for a quick release of Fannie Mae and Freddie Mac, you might want to exercise some patience.

While the odds of the pair exiting conservatorship increased sharply once Trump’s second term began, it still faces an uphill battle.

One of the major sticking points is mortgage rates, which many expect to increase if they’re released.

Having a near-explicit guarantee that Fannie and Freddie will buy and securitize mortgages makes them cheaper for consumers.

The expectation is if/when they go public, mortgage rates would need to be higher to compensate for increased risk.

Fannie and Freddie Have Been in Conservatorship Since 2008

First some quick background. After the worst housing crisis in recent history, Fannie Mae and Freddie Mac, known as the government-sponsored enterprises (GSEs) were placed in conservatorship.

This was essentially a government bailout as the pair were “severely damaged” as a result of the early 2000s mortgage meltdown and “unable to fulfill their missions without government intervention.”

The arrangement allowed them to continue to support the very fragile housing market as it recovered over the past decade.

But perhaps nobody expected the pair to remain in government hands as long as they have.

At last glance, it has now been nearly 20 years! Of course, this isn’t the first time efforts have been made to release them back into the wild.

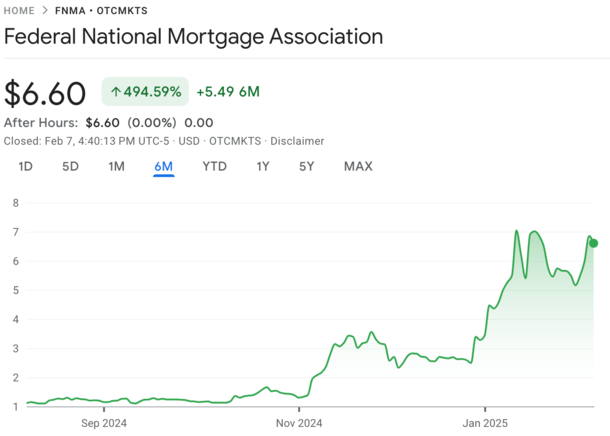

During Trump’s first term that began back in 2017, there was a lot of talk of a release. And the stocks of both companies responded accordingly.

They were trading in the $1 range in late 2016 and quickly increased to more than $4 per share in early 2017 before fading again.

Once the privatization of Fannie Mae and Freddie Mac lost steam, they eventually became penny stocks.

Lots of Investor Speculation Surrounds Their Release

Like eight years ago, there’s been a lot of investor speculation surrounding their release, which arguably is part of the problem.

It seems folks are more interesting in making a buck on a trade than considering the actual implication of their release. Go figure…

The latest speculator to get in on the apparent gold rush was investor Bill Ackman, whose Pershing Square Capital Management firm “could own about 180 million common shares of the two companies.”

And he could reportedly see a $1 billion gain on the investment, with the shares potentially climbing to around $34 post-IPO.

For reference, they currently trade at around $6 each, so it would represent quite the gain.

Similar to conditions prior to Trump’s first presidential victory, the pair were trading in the $1 range.

But they have since skyrocketed, with both FNMA and FMCC up roughly 500% since Trump won a second term and speculation about their release reached euphoric levels.

As noted, this is the conflict of interest currently in play. And the same issue we saw eight years ago. It’s a stock trade instead of a “Hey, is this good for our country?”

Fannie and Freddie’s Release Will Hinge on Impact to Mortgage Rates

While investors are hoping the pair get released and make them untold riches, we should only release them when it is safe and appropriate to do so.

If newly-appointed Treasury Secretary Scott Bessent, who is incidentally also the new acting director of the Consumer Financial Protection Bureau (CFPB) does the right thing, that might not be for some time.

In an interview with Bloomberg this week, when asked about their release, Bessent said, “Right now the priority is tax policy. Once we get through that, then we will think about that.”

He added that “The priority for a Fannie and Freddie release, the most important metric that I’m looking at is any study or hint that mortgage rates would go up.”

“So anything that is done around a safe and sound release is going to hinge on the effect of long-term mortgage rates.”

Simply put, he and those around him are aware that mortgage rates will likely rise if Fannie and Freddie are forced to stand on their own.

And because mortgage rates have surged from around 3% to start 2022 to roughly 7% today, the last thing the Trump administration wants is higher rates.

So really it boils down to helping investors get rich or helping everyday Americans buy homes with lower mortgage rates.

Will be an interesting decision…

The Pair Should Be Released, But Perhaps Slowly After They Reduce Their Footprint

My thoughts on the matter are that the pair aren’t ready to be released. Not much has changed since they went under conservatorship, other than mortgage quality vastly improving.

Sure, they don’t have nearly as many worries about mortgage defaults and foreclosures, but they also continue to back the vast majority of home loans in the United States.

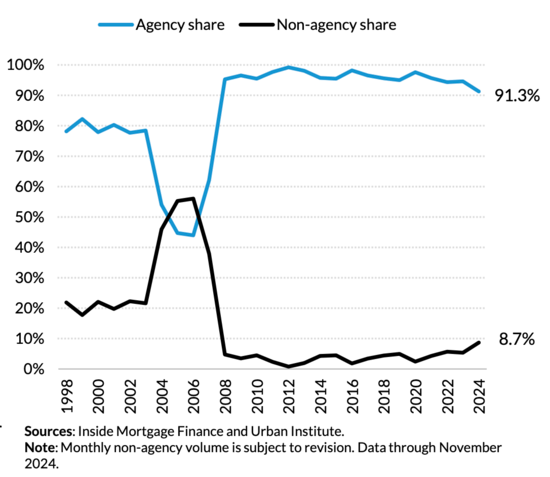

Look a the chart above from the Urban Institute. More than 91% of MBA issuance is agency-backed, which does include FHA and VA too. But about 40% of first-lien originations are GSE, while just 4.1% is private-label.

Without them, there would be chaos in the mortgage market. Even if released, there would likely be chaos.

However, they should be released at some point if they are truly public companies, and not government entities.

A better way about going about it might be greatly reducing their footprint before that happens (sorry investors).

To do so, they can pull back or completely stop buying and securitizing mortgages tied to second homes and investment properties.

In other words, limit their options to primary residences for everyday homeowners as opposed to those who are buying a second, third, fourth, or even fifth home.

Ironically, this could also free up for-sale supply, which has plagued the housing market for at least the past decade.

There could be additional changes to their product menu, which would make it smaller, with the implied purpose of ushering in more private capital to the mortgage market.

As Fannie and Freddie got smaller, private players could grow larger and play more of a role.

This would reduce our reliance on the pair, and lessen the impact of their eventual release.

(photo: Virginia State Parks)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.