File this one under unintended consequences of a global trade war.

When you start a trade war, or at least threaten one, unexpected things can happen.

We already got the sense that mortgage rates don’t like the trade war because of all the uncertainty involved.

But there’s another wrinkle to consider here as well, and that’s the massive holdings of mortgage-backed securities (MBS) held by foreign countries.

Should they decide to sell as a result of tariffs imposed against them, mortgage rates could jump in the United States.

Foreign Investors Own a Good Chunk of Our Mortgages

First things first, let’s talk about why foreign investors hold our mortgages and how much they own.

In general, foreign countries invest in the United States for the perceived soundness and safety of its assets (and debt).

Sure, things didn’t go so well in 2008, but all in all, foreign investors have long invested in agency mortgage-backed securities (MBS) because they’re relatively safe, high-yielding investments.

And they’re pretty much guaranteed as well.

Agency MBS include loans backed by Fannie Mae and Freddie Mac (conforming loans), which have an implicit government guarantee.

And government loans, such as FHA loans, VA loans, and USDA loans, which have an explicit guarantee.

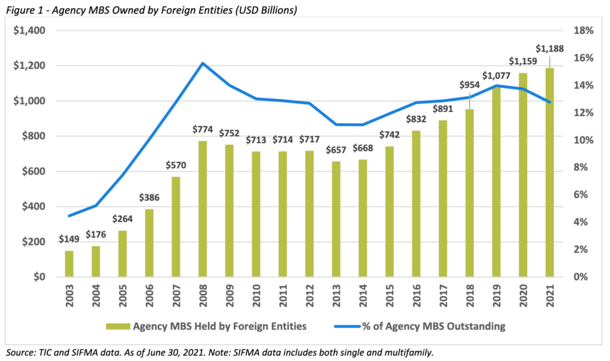

Per Ginnie Mae, which provides a guarantee for the government home loans, foreign holdings of agency MBS hit an all-time high of roughly $1.2 trillion in June 2021, representing nearly 13% of the market.

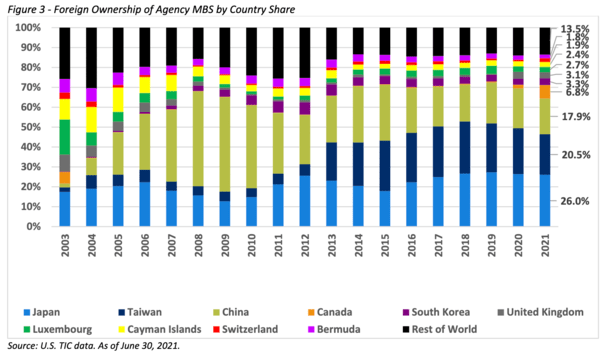

The biggest investors of our agency MBS are Japan, Taiwan, and China, with Canada recently becoming the fourth-place foreign holder.

The so-called “Big 3” accounted for about 64% of agency MBS foreign holdings, with another 22% coming from the rest of the top 10.

In other words, foreign holdings of agency MBS are concentrated in just a few countries. And it just so happens that we’ve been slapping them with tariffs lately.

Could These Countries Sell Their MBS Holdings in Response to Tariffs?

There is now at least some concern that these countries could sell their MBS holdings in response to the tariffs and wider trade war.

After all, if it could potentially hurt us in the process, it could be used as a sort of bargaining chip to fend off the tariffs.

This scenario was brought up in a recent BTIG report, as noted by Inside Mortgage Finance this week.

While it’s all speculative, anything is possible and on the table at this point. China, Japan, and Canada have been hit with tariffs. And Taiwan has been threatened with tariffs.

Japan called it “regrettable” that they weren’t excluded from the steel and aluminum tariffs, while China levied tariffs and Canada imposed countermeasures against the United States.

It hasn’t spilled over into other areas, like MBS holdings, but given how much they own, there are fears these countries could dump their investments en masse.

If that were to happen, the market would ostensibly be flooded with MBS, which would increase the supply and lower the price.

Increased Supply of MBS Would Lead to Higher Mortgage Rates

The best way to track mortgage rates is with MBS prices. When their prices go up, mortgage rates come down. And vice versa.

Assuming these countries, or just one them, decided to sell a ton of MBS, prices would come down.

After all, more supply than demand leads to lower prices.

How much they’d fall is another question, but it would put increased upward pressure on mortgage rates.

Perhaps rates on the 30-year fixed would go up another 0.25%, who really knows?

Ultimately, you’d need a buyer to come in and absorb that excess supply to avoid a major price disruption.

Perhaps that’d be the Fed if things got really bad, assuming this type of thing even transpired.

In a sense, it could lead to another round of Quantitative Easing (QE), where the Fed became a buyer of MBS, thereby increasing their price and lowering mortgage rates.

Of course, these countries likely wouldn’t want to sell their holdings on the cheap, while also hurting their own economy in the process.

They rely on the value of the U.S. dollar to manage their own currency and balance trade, so it’d possibly be counterproductive to do so.

In the end, it’s kind of a silly thought, but it does illustrate just how much uncertainty there is in the market.

And why mortgage rates will have a tough time moving substantially lower, even if economic data justifies it, until we get more clarity on the ongoing trade war.

Read on: Tariffs vs. Mortgage Rates

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.