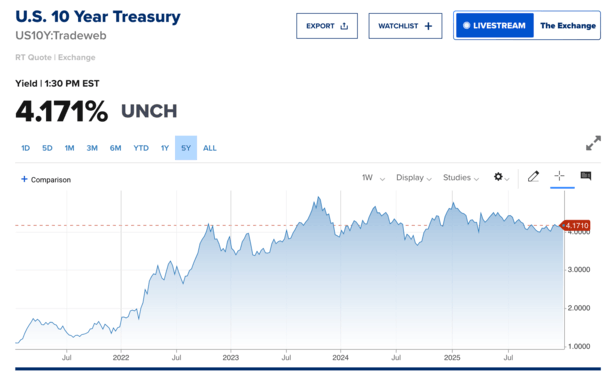

One of the key ways to track mortgage rates is to look at the 10-year bond yield.

It acts as a bellwether for 30-year fixed mortgage rates because most home loans only last for about a decade.

They are typically paid off ahead of time, whether it’s due to a home sale, a refinance, or perhaps prepayment via extra payments or a lump sum payoff.

But because mortgages are riskier than Treasuries that are guaranteed by the government, there is a spread between the two.

This spread ensures MBS investors get a higher return for taking on the risk of mortgages defaulting or being prepaid.

And lately this spread has come in tremendously, leading to the lowest mortgage rates in about three years.

Normal Mortgage Spreads Lead to the Best Mortgage Rates in Three Years

To come up with the spread, you simply subtract the current 10-year bond yield from the daily mortgage rate (of your choosing).

For example, if you use Mortgage News Daily’s widely cited 30-year fixed average of 6.01% today, and a 10-year yield of 4.18%, we get a spread of 1.83 basis points (bps).

For context, the historical spread between the 30-year fixed mortgage and 10-year Treasury is about 170 basis points.

In other words, mortgage spreads are basically back to normal right now.

The reason mortgage rates were so much higher a year ago (and even higher in late 2023) was due to really wide spreads.

At one point, the spread was around 325 bps, meaning MBS investors would only buy mortgage-backed securities if they could earn a really sizable return relative to Treasuries.

One of the reasons was after the Federal Reserve stopped buying trillions in MBS via QE, there was a demand vacuum.

Essentially, mortgage rates shot higher due to greatly reduced demand and as they did, MBS investors shied away due to increased default risk and also the thought of higher prepayment risk.

There was less liquidity and at the time, there was a strong opinion that the 8% mortgage rates wouldn’t last very long.

Chances are they’d be refinanced in short order once rates normalized. And guess what? They were right.

A lot of 2023- and 2024-vintage mortgages only lasted a year or two before being refinanced to much lower rates.

MBS investors don’t like when high-rate loans are quickly paid off and exchanged with lower-rate loans.

So they required a higher spread than normal at the time to compensate for this increased risk.

Why Are Mortgage Rate Spreads Better Now?

Today, mortgage rate spreads are basically back in a totally normal range, which is wild considering they were nearly double that in 2023.

But now that the MBS market has adjusted and comes to terms with the new post-QE normal of mortgage rates around 6%, there’s a lot more certainty.

In essence, rates are historically pretty average and there’s the thought they could hang around these general levels for the foreseeable future.

If that’s the case, there’s the argument that the loans will no longer be paid off rapidly and there’s a sense of stability for MBS investors.

It’s also a pretty decent yield for MBS investors to earn ~6%, especially if they think they’ll continue to earn 6% for a longer period of time.

As noted, the 8% rates were very short-lived, so while the higher rates may have seemed attractive, a wider spread was required at the time because many investors probably had a feeling it wouldn’t persist.

Now that we’ve had mortgage rates remain in a tighter range for the past year and a half, there’s more demand again. Investors have re-entered the picture.

In addition, as you likely heard, Trump ordered Fannie Mae and Freddie Mac to purchase $200 billion in MBS to bring spreads down even more.

That’s why they tightened up further over the past couple days, despite the 10-year bond yield barely budging during that time.

How Do Mortgage Rates Move Even Lower?

While the news on spreads is a positive, it also means we likely won’t get much more relief via spreads.

After all, they are back to normal. So the only way to get mortgage rates even lower (outside another round of QE) is via a lower 10-year bond yield.

Remember, it serves as a bellwether, so if the 10-year comes down, 30-year fixed mortgage rates can come down too.

But in order for that to happen, you either need inflation to cool or you need labor to worsen.

You could have both those things happen concurrently, which is kind of what’s been happening lately.

The spreads were a major reason why mortgage rates got markedly better, but we can also thank lower 10-year bond yields too.

The 10-year yield was priced at about 4.65% a year ago and is nearly 50 basis points lower today.

So mortgage rates are about 1.25% lower today (7.25% vs. 6%) thanks to both a lower 10-year bond yield and tighter spreads.

But if spreads are normal, you look to bond yields if you want even lower rates. As noted, that can happen with a slowing economy, whether it’s disinflation or higher unemployment.

The trick is threading that needle where inflation cools and labor perhaps eases without a recession, so we don’t get lower mortgage rates but a worse off economy (and by extension housing market).

Read on: 2026 Mortgage Rate Predictions

(photo: BricksFanz.com)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.