There’s a lot going on right now with mortgage rates so I’m dedicating a very long post to it.

First and foremost, mortgage rates are dropping fast as the economy teeters on the brink of a possible recession.

The driver is worldwide tariffs and a global trade war, which has led to a stock market crash and a flight to safety in bonds.

When bonds see more demand, their yields fall and so too do mortgage rates.

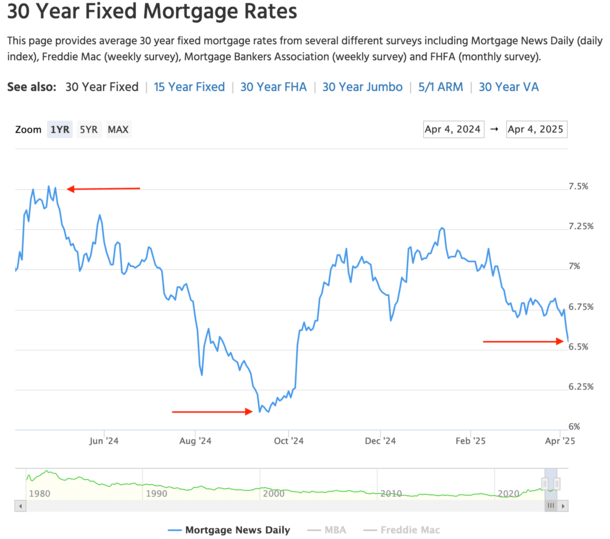

As a result of the calamity, the 30-year fixed has fallen about 25 bps (0.25%) from 6.75% to 6.50% this week. And could come down even more.

Global Tariffs and a Trade War Are Good for Mortgage Rates, But Maybe Not Anything Else

In the past week, the 30-year fixed has fallen from around 6.75% to close to 6.50% today, at least according to MND.

Every lender will have different pricing, but it’s clear the trend has been lower. A lot lower in the past week.

And it could just be getting started given the turmoil in the financial markets, with stocks now close to entering bear territory.

When this happens, investors seek the safety of bonds, and mortgage rates benefit because they’re backed by similar securities (albeit with more risk).

So if you’re wondering why mortgage rates dropped, you can thank the global tariffs, trade war, and plunging stock market.

Even a decent jobs report released this morning wasn’t enough to avert a market selloff, as all eyes are on the trade war now.

There’s also now an expectation that the Fed might ease its own fed funds rate sooner and cut even more if this persists.

Of course, at what great cost? The cost of the economy? A recession? A depression? The drop in rates might not be without a lot of negative consequences.

Simply put, be careful what you wish for. Sure, lower mortgage rates are a gift for homeowners who can benefit from a refinance. Or a home buyer looking for improved affordability.

But only if they can actually make the payment each month. The longer this goes on, the more job losses we’ll see.

If things get really bad, we could also see downward pressure on home prices at a time when affordability is already rock bottom.

So you might get a lower mortgage rate but also a lower home price, not that it necessarily matters unless you need/want to sell anytime soon.

Still, there are larger stakes here, and mortgage rates don’t exist in a vacuum, nor are they the be all, end all.

Will Mortgage Rates Keep Dropping?

They’ve fallen about 25 basis points (0.25%) in the past week, which is a strong move lower in the span of just one week.

And they might not be done dropping, as Trump and Treasury Secretary Scott Bessent have repeatedly said lower interest rates are a big priority.

Of course, they didn’t tell everyone the economy (and stock market) might also come down as a result.

Right now, I’d say the trend is our friend, assuming lower rates is what you’re looking for.

But big rate moves lower can often be stopped in their tracks with little or no warning.

Another important consideration is that mortgage lenders are slow to lower rates, but quick to raise them.

Give them ANY reason to raise rates and they’ll do it. Conversely, they’ll cautiously lower them if there’s reason for them to drop.

This means there’s still room for rates to continue falling, especially if the trade war persists or worsens.

And keep in mind that rates are still mid-6s, which is better than recent levels, but a far cry from the rates we saw a few years ago.

Combined with a deteriorating economy, it might not be all it’s cracked up to be.

Keep It In Perspective

Another important point to make here is that mortgage rates are still pretty high relative to where they were just a few years ago.

Remember, the 30-year fixed was low-3s (even sub-3%) in early 2022. And rates were in the low-6s as recently as September and October of last year.

This is why I’ve mentioned that Bessent and Trump didn’t do much to lower mortgage rates.

If you recall, they were lower right before the election and simply jumped once Trump became the frontrunner, as his policies were expected to be inflationary.

So a rate of 6% today isn’t necessarily fantastic if we zoom out and look at the bigger picture.

And the 30-year fixed remains a long, long way from the lows seen for much of the past decade.

Of course, if this keeps up, mortgage rates could inch closer to those levels. And any little bit helps, right?

It’s clear that housing affordability is historically poor, and the easiest lever to improve purchasing power is lower interest rates.

While home prices can also provide some relief, lower rates do a lot more for the monthly payment.

For example, a 1% drop in rates is equal to about a 11% drop in prices.

What It Means for Prospective Home Buyers

This is a tricky one because on the one hand, lower mortgage rates are obviously a good thing.

They mean a prospective home purchase is now cheaper. For example, mortgage rates were 7.50% in April 2024.

If they keep trending lower, or even stay at these levels, they’ll be about a full percentage point lower.

On a hypothetical $500,000 home purchase with 20% down payment, the payment is $2,796.86 at 7.5% versus $2,528.27 at 6.5%.

That’s a difference of nearly $270 per month, which is nothing to sneeze at. So there’s clearly some payment relief there, especially if the loan amount is even larger.

And as I’ve said time and time again, there isn’t a historical inverse relationship between home prices and mortgage rates.

Meaning that the theory prices will rise if rates fall isn’t true. Both prices and rates can fall in tandem.

As such, you could be looking at a lower interest rate AND a lower sales price. Win-win, right?

Well, there’s one small hitch. The economy.

Yeah, if rates are only coming down because of economic calamity, it’s not the best situation, especially if you’re buying a home.

It could mean that home prices are due to fall even more, or that your job security could come into question.

Doesn’t matter much if the rate is 1% lower if you can’t make the mortgage payment, period.

Simply put, only those who are well-positioned financially with stable employment should view the current situation favorably.

If you’re at all worried about your job security, you might want to continue renting if you’re not yet a homeowner.

Simply put, look at the big picture, not just the lower interest rate. And as I pointed out last month, expect to hold your property for a long time if buying today.

The reason is mortgage repayment has slowed tremendously, and if price appreciation does too, you won’t be able to sell for a profit or even break even when factoring in selling costs.

At the same time, don’t attempt to time the market by waiting for mortgage rates to drop before buying a home.

Apply the same principles as always because homeownership is a serious commitment.

What It Means for Existing Homeowners

If you’re already a homeowner, especially a recent home buyer, this could be a good opportunity to apply for a rate and term refinance.

But similar to September/October, the big question is do you lock in a rate now, or do you float your rate or even wait for rates to come down even more?

Back then, there was an expectation that rates were going to keep falling, and so many home buyers and existing owners looking for payment relief waited.

Many missed the boat as a result, as rates jumped in mid-October and didn’t look back as they surged from around 6% to 7.25%.

The opportunity has presented itself once again, so the question is will homeowners react differently?

What’s enough of a rate discount to make a refinance worth it? I don’t believe in refinance rule of thumb, as every scenario is unique.

So if you’re in a position to possibly benefit from a refinance, take the time to run the numbers for your particular loan scenario.

Speak with a few loan officers and mortgage brokers to see how much you stand to save, and whether it makes sense to wait or make a move.

While not necessarily ideal, you can always refinance a second time later (assuming you still qualify) if rates come down a lot more later.

If you’re selling a home right now, it might lead to an uptick in demand, though some buyers may also get cold feet. Ultimately, it’s too early to know what the net effect will be.

Beware of the Mortgage Rate Bounce

One last thing. Often when there’s stock market carnage, like there is now, there’s a bounce day. Basically, the selloff runs out of steam and bargain hunters enter the fray.

Then stocks make up some of the damage, though it’s often short-lived and only makes up a small portion of the shortfall.

Mortgage rates also tend to experience pullbacks if they drop a lot in a short window of time, as they have recently.

So it’s entirely possible that we might see a day next week where mortgage rates jump back up.

In other words, a rate quote of say 6.25% today might be 6.375% next week, or even higher.

It really all depends on what transpires, and nobody has a crystal ball. One of my chief concerns, when it comes to a mortgage rate bounce, is negotiating on tariffs.

If the Trump administration and these countries decide to pull back on the tariffs, the selloff could easily reverse.

Those who jumped into bonds might head back into stocks, and the 10-year bond yield could go up again, pushing mortgage rates higher in the process.

The biggest factor in my opinion will be the tariff negotiations with China. I fully expect the other countries to work out deals ASAP.

But the China situation might be a tougher nut to crack and could persist for some time, if not indefinitely. Who knows?

Either way, expect a ton of volatility if you’re in the market to get a home loan. Rates will likely bounce around a lot, even if they continue to fall as the year goes on.

It’s never a straight line up or down, so adjust your expectations accordingly and pay attention to what’s going on in the news!

Read on: How to easily track mortgage rates with MBS prices and bond yields.

(photo: k)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.