There’s a saying known as “sell the news,” in which traders position themselves on a well-known rumor, then unwind once the news hits.

That rumor could be a Fed policy decision, widely expected to be a 25-basis point cut tomorrow.

And those traders could be bond traders, who have been buying up 10-year Treasuries in anticipation.

But once that news is disseminated, you might see a sell off of sorts, especially if there had been a lot of movement leading up to the news.

One could argue that mortgage rates have been on quite a run lately, and thus a pullback tomorrow wouldn’t be totally out of the question.

Will Mortgage Rates Experience a Sell the News Moment?

First let me preface this by saying you shouldn’t try to time the market, or predict mortgage rates.

It’s very difficult if not impossible. Many have tried, many have failed. But it’s fun to discuss possible outcomes, especially since the media loves to chime in on the subject.

So let’s dive in.

One helpful thing we can do is look at mortgage rates in the lead up to a Fed rate decision.

Over the past three months and change, the 30-year fixed has fallen from above 7% to around 6.25%, per the latest data from Mortgage News Daily.

In just the past month, the 30-year fixed has dropped from around 6.60% to 6.25%. That’s a pretty big move lower.

Of course, I should note that this hasn’t happened because of the Federal Reserve. It was driven by several weak labor reports and massive downward revisions to prior reports.

It has been a labor market story, with worries the economy could be slowing and slipping into a recession.

It just so happens that the Fed is releasing its highly-anticipated FOMC statement tomorrow.

And because of that awful jobs data, it’s basically a given that the Fed will cut its federal funds rate 25 bps.

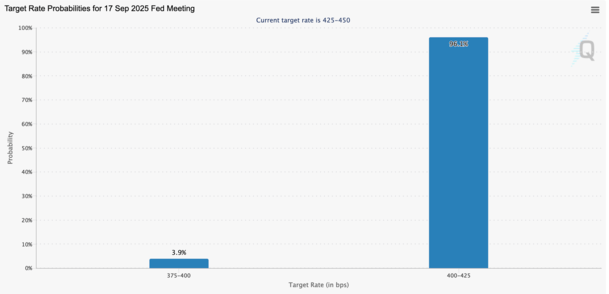

In fact, CME has a 25-bp cut at 96.1% odds today, with the remaining 3.9% tied to a less likely 50-bp cut.

The takeaway is this Fed rate cut is a sure thing and has been for a while, so it’s not going to come as any surprise to anyone tomorrow.

To my point about selling the news, we could see a bounce in 10-year Treasury yields tomorrow simply as the news is confirmed.

Especially since bond yields are teetering just above 4%, and were closer to 4.50% as recently as two months ago.

The Past Two Rate Cuts Resulted in Totally Different Outcomes for Mortgage Rates

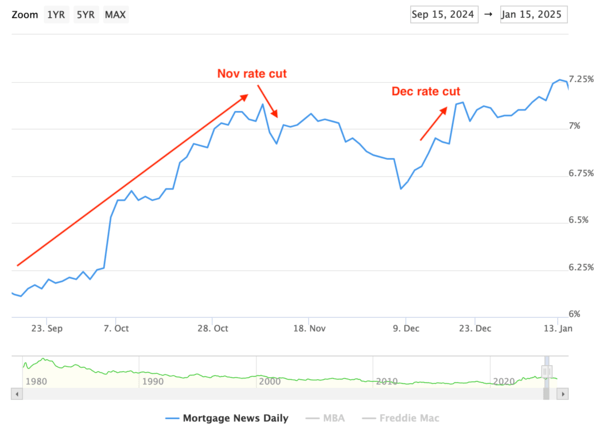

Now let’s take a look at the past two rate cuts, which took place on December 18th, 2024 and November 7th, 2024.

Those were both 25-bp cuts, same as the one expected tomorrow.

The December cut led to a big jump in mortgage rates, but that may have been driven by the release of the quarterly dot plot, which was more hawkish than expected.

Mortgage rates had also fallen quite a bit leading into that Fed meeting, so a bounce wasn’t totally surprising.

How about the November rate cut? Well, that was a different story. On November 7th, mortgage rates had one of their best days in years.

However, let’s consider the build-up. The 30-year fixed had risen about one full percentage point in the span of just months before the cut!

From about 6.125% in mid-September to 7.125% in early November, which was quite the meteoric rise (ironically that started after the Fed cut 50 bps in September).

So it lends credence to the idea that context matters and that the sell the news thing could be a factor.

Obviously, it also depends what happens on the day, if there’s some other event or economic data.

But if we apply this logic, and note that the 30-year fixed has fallen significantly leading up to this cut, a bounce higher would be expected.

The one caveat is the Powell press conference tomorrow. If he says dovish stuff, mortgage rates might rally even more.

There’s also the very slim possibility of a 50-bp cut, which could also shake things up. But chances are we might see a little uptick once the news is announced.

Still, mortgage rates are the best they’ve been in about a year and could get even better from here, even if there are some ups and downs along the way, as there always are.

Read on: Fed Rate Cut, But Mortgage Rates Up: What Gives?

(photo: romana klee)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.