United Parcel Service (NYSE: UPS) is an interesting dividend growth stock. It yields 6.4%, and the company has raised its dividend every year for 16 years.

But UPS is in the process of a big transition.

It is disentangling itself from Amazon, its largest customer.

You might think, “Why in the world would they do that?”

While delivering packages for Amazon is high-volume, it is also low-margin. UPS is sacrificing the revenue from Amazon going forward in order to focus on more profitable business.

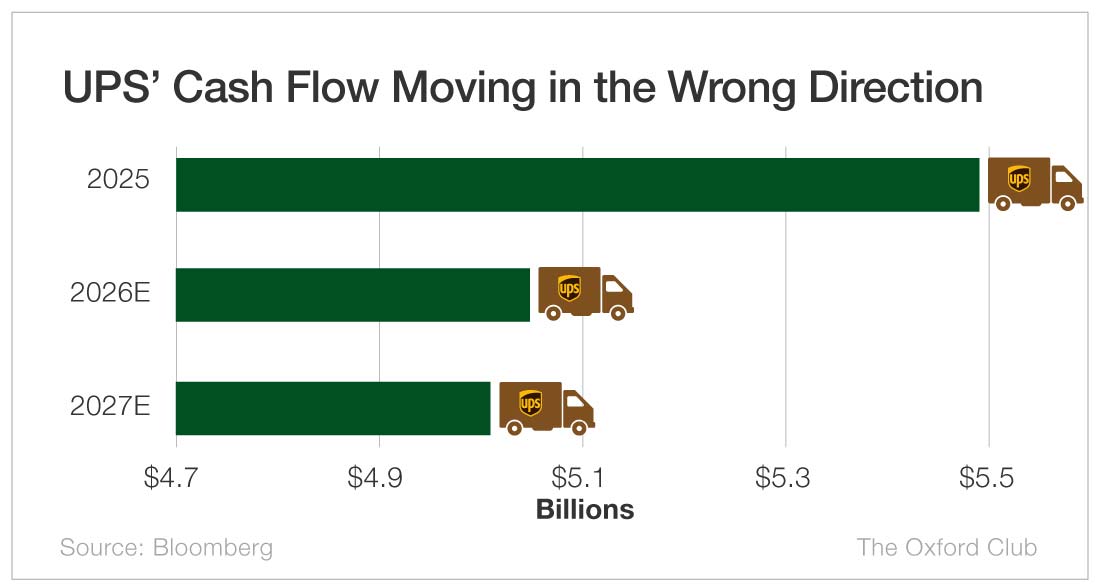

That will lead to a decline in free cash flow in the near term.

Last year, UPS’ free cash flow was $5.47 billion. It is forecast to be $5.05 billion this year and fall to $5.01 billion in 2027.

That’s a problem. Declining free cash flow causes companies’ Safety Net ratings to drop.

Another issue is that the payout ratio is too high.

Last year, UPS paid shareholders $5.4 billion, or 99% of its free cash flow. In 2026 and 2027, the payout ratio is projected to exceed 100%.

That means the company is paying shareholders more in dividends than it is generating in free cash flow.

That’s no good.

In fact, Safety Net only accepts a 75% or lower payout ratio before it starts downgrading stocks.

Though UPS has boosted its dividend for 16 years in a row, it is unlikely to do so this year as it goes through this transition.

But management knows it has a lot of former employees as shareholders since it was an employee-owned company prior to 1999. As a result, Brian Dykes, UPS’ chief financial officer, stated, “When we look across our shareholder base, we recognize that the dividend is important, right? And so we will protect the dividend.”

Now, Safety Net doesn’t care what a CFO says. It goes by the numbers.

Falling free cash flow and a payout ratio over 100% mean the dividend is not safe. For that reason, UPS gets a low mark for dividend safety.

However, I don’t expect a dividend cut in the next 12 months. If free cash flow is worse than expected this year, that could lead to a reduction in 2027, though I do believe management will do everything it can to avoid it.

Of course, if the company is able to become more profitable as a result of this transition away from Amazon, that could boost its free cash flow, which would greatly improve its dividend safety.

Dividend Safety Rating: F

What stock’s dividend safety would you like me to analyze next? Leave the ticker in the comments section.

You can also take a look to see whether we’ve written about your favorite stock recently. Just click on the word “Search” at the top right part of the Wealthy Retirement homepage, type in the company name, and hit “Enter.”

Also, keep in mind that Safety Net can analyze only individual stocks, not exchange-traded funds, mutual funds, or closed-end funds.