Mortgage rates have had a pretty good April, all things considered.

They’ve come down about 30 basis points (0.30%) over the past month, despite the conflict in Iran still raging on.

So I was curious where mortgage rates would be without a war in Iran, had it never gotten started at the end of February.

Back then, we were just below 6% for a 30-year fixed and apparently we’d still be there had history been different.

And while the difference in monthly payment might be negligible, the psychological factor could have been huge for home buyers this spring.

Mortgage Rates Have a 0.25% ‘Geopolitical Premium’

I asked xAI’s Grok where mortgage rates would be sans the conflict in Iran and it told me about a quarter-point lower.

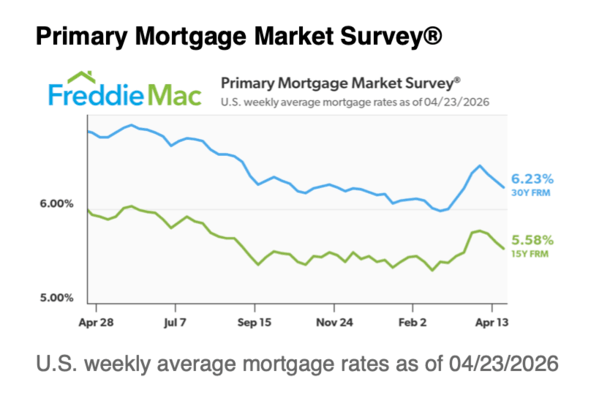

If we use Freddie Mac’s latest 30-year fixed reading of 6.23%, that would put the popular loan type right below 6%.

Instead, borrowers are still facing rates well into the 6s, which even if not a big payment difference, must not feel as nice as a 5-handle rate.

There’s a reason most prices end in .99. It’s no different with mortgage rates.

Home buyers would much rather have a 5%-something versus a 6%-something. It just looks better. And I’m sure it feels better too.

Instead, those who’ve been buying homes this spring have had to settle for the higher rates, assuming they didn’t buy down the mortgage rate.

As for why, it’s what Grok coined as a “geopolitical premium” of about 25 bps.

Here’s how it breaks down:

- Pre-conflict 30-year fixed mortgage rate: 5.98%

- Minus embedded geopolitical premium today (~25 bps)

- Plus/minus modest natural drift (0–10 bps lower)

- Mortgage rate range: 5.85% to 6.05%

- Midpoint guess: 5.95%.

Mortgage Rates Usually Fall During Uncertain Times

Typically, mortgage rates fall when there’s a war because there’s a flight to safety in bonds.

Investors seek a safe haven in uncertain times. This time is different.

We have a stock market at/near all-time highs as investors continue to chase higher returns in the face of $105+ per barrel oil.

So really it’s not so much a geopolitical premium as it is an energy price premium, given oil was closer to $70 per barrel pre-conflict.

If we consider the 10-year bond yield, it was just below 4% prior to the war with Iran, and now sits around 4.30%.

This means it’s mostly the difference in yields pushing 30-year fixed mortgage rates higher, and a little bit of the spread widening.

The next question is when can mortgage rates return to pre-war levels? That’s a tougher one to answer because the path remains very unclear.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.